The Federal governments mid-century housing policies, as expressed through the Federal Housing Administration, as well as the Housing Acts of 1937, 1949, and 1954 structured much of the country’s housing stock. The suburbs were subsidized and segregated with Federal dollars, as were public housing developments in inner cities. Black neighborhoods were bulldozes under the auspices of “slum clearance” and “urban renewal,” as Federal officials tried to combat “blight,” a form of urban decay that went from a planner’s term of art into a perceived national crisis as the Great Migration drew more black people into urban areas. Many of the policies relied on the Chicago School of sociology, which argued that cities had “natural” life paths that government had to work with in order to achieve desirable outcomes. In practice, that meant subsidizing areas where white people moved, while disinvesting in mixed race or black neighborhoods.

1936: FHA Underwriting Manual

The Federal Housing Administration provides mortgage insurance for home loans, and it has since it was created during the New Deal. Mortgage insurance makes it less risky for banks to extend credit to purchase homes. The suburban expansion of the mid-century was subsidized through the FHA, and to a lesser extent the Veterans Administration, which also backed loans. Thus, the underwriting manual is a key for unlocking what kinds of property could be easily financed on good terms.

The manual was written by a man named Frederick Babcock, a Chicago real estate man. He saw himself as bringing “scientific method of thought and analysis” to real estate appraisal. The FHA (along with the Home Owners’ Loan Corporation) helped to standardize the terms and conditions of a mortgage. Rates became fixed and their terms extended to as much as 30 years. That lowered the upfront costs of buying a home tremendously.

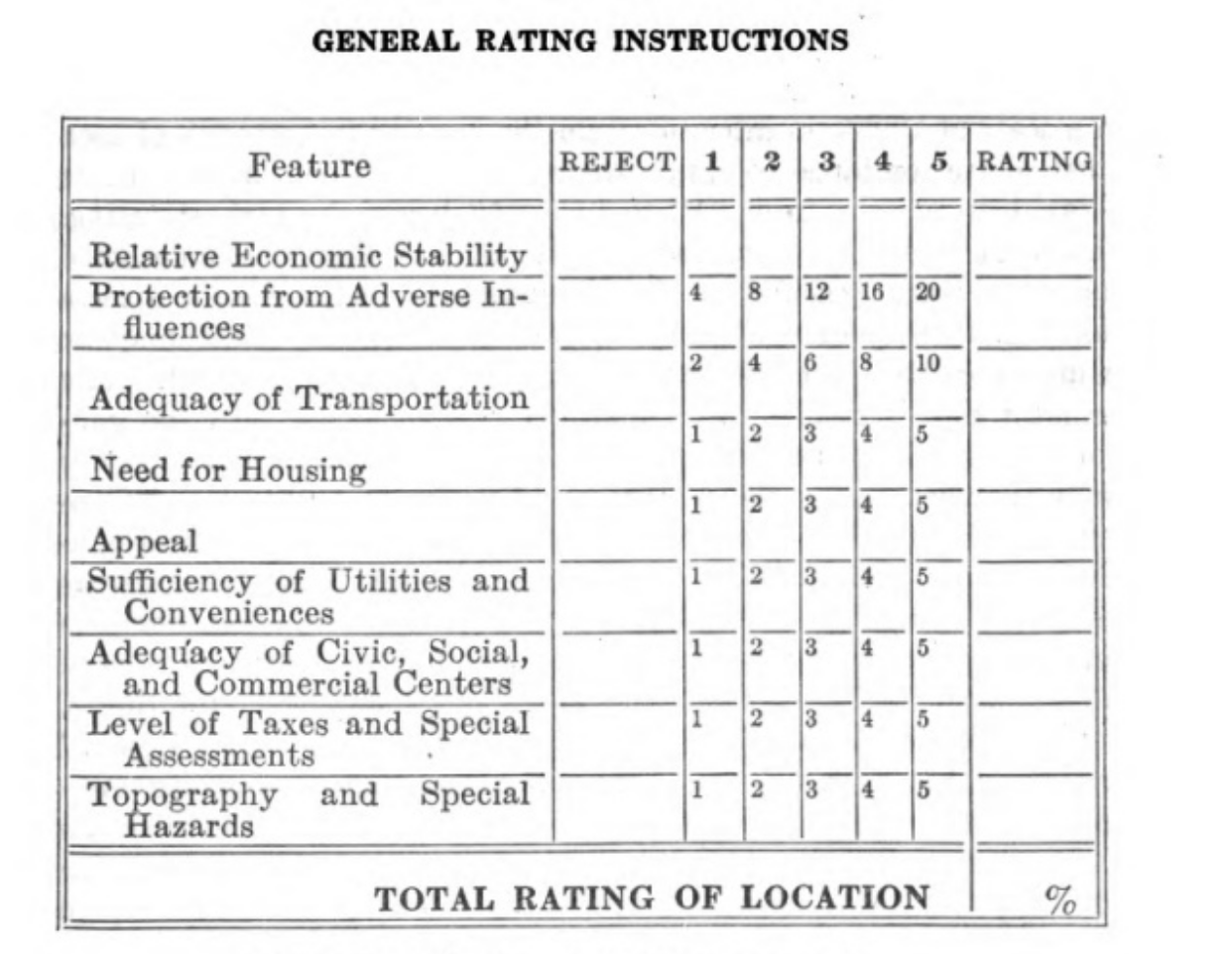

But if you were going to make loans for 30 years, then you had to be sure that the loans would be good for that long. Given that neighborhoods changed, a core component of an FHA analysis of a loan’s potential was not the buyer or the home, but the location of the home. They developed a system of “risk rating” different neighborhoods.

Drawing on Chicago School sociology and real estate rules of thumb, Babcock baked anti-black racism directly into the underwriting of the FHA in a myriad of ways. “Racial heritage and tendencies seem to be of paramount importance,” Babcock believed, in that they “largely determine the extent to which [the people] develop the potential value of the land.”

The FHA created “underwriting grids” with a complicated scoring system that worked like an algorithm. Each borrower, property, and property location received a rating which was, itself, composed of a variety of factors. For each of the domains, a perfect score was 100, and anything under 50 rated a rejection. Within the location rubric, there were 9 factors ranging from “Protection from Adverse Influences,” the most important, to a range of less important factors, like “Sufficiency of Utilities and Conveniences.” An adverse influence, of course, could be an inharmonious racial group or, say, a copper smelter or brewery. A high score across the board meant longer mortgage terms and lower interest rates. Low scores meant, at worst, no mortgage insurance would be provided, or at best, that the terms of the loan would be worse.

While the scoring system looks complicated, and presaged the kind of algorithmic discrimination that has come under intense scrutiny in recent years, the unmistakable stank of humanity remained on the system. Valuators didn’t have to complete the whole process, if they decided that the risk of any one component was too high. Then, they could write REJECT on the total rating and be done with it.

But they didn’t need to get very fancy with neighborhoods like West Oakland, or many other black neighborhoods near the nation’s downtowns. The very first rule of rating locations stated that “the slum and blighted areas which almost invariably surround downtown sections of major cities” were to be put into “downtown reject areas.”

“Downtown reject areas must be outlined with the greatest of care in order to save the embarrassment to the Insuring Office in connection with applications on mortgages which lie within such borders,” the Underwriting Manual holds. Central downtown core areas include the business and commercial sections of the cities as well as the slum and blighted areas which almost invariably surround downtown sections of major cities.

Section 233 of the 1936 Underwriting Manual advised valuators to “investigate areas surrounding the location to determine whether or not incompatible racial and social groups are present, to that end that an intelligent prediction may be made regarding the possibility or probability of the location being invaded by such groups.” The FHA was blunt about what they thought racial change did to a neighborhood. “A change in social or racial occupancy generally leads to instability and a reduction in values,” it read. To the FHA, there could be no stable, integrated neighborhood.

1949: Housing Act of 1949

President Harry Truman got the Housing Act of 1949 through Congress thanks to an intense housing shortage. It allocated $1.5 billion in loans and grants for urban redevelopment, expanded FHA mortgage insurance, and called for the construction of 800,000 public housing units. Planners and housing reformers dreams were coming true, it seemed. You’d bulldoze, but you’d build back better. Neighborhoods wouldn’t be destroyed, but rebuilt. Housing, as a whole, would be improved.

The Act touched off a flurry of activity as cities tried to get a piece of the Federal public housing money that was now available. One stipulation was tricky: cities had to raze a unit of substandard housing for every unit of new public housing that was built.

Ultimately, the large-scale construction of public housing would be crippled, and by 1954, with Republican Dwight Eisenhower in power, cities would turn to “urban renewal,” which used public power to deliver huge portions of cities to private developers, often displacing non-white people in the process.

1954: Housing Act of 1954

The first glimmers of what came to be called “urban renewal” were hopeful—a city was to be “renewable,” in the same sense as renewable energy. Millions of people lived in terrible, deteriorating housing. It had be to fixed. But for every good intention, there were other motives at play. Nationally, downtown business owners realized that the decentralization of the city, which the FHA and other government projects were encouraging, threatened their enterprises. But if a slum was cleared and replaced by public housing, it would not return rich people to the city, which is what they wanted.

As the historian Robert Fogelson put it, big downtown businesses needed “a form of slum clearance that would wipe out not the worst slums, but rather the run-down neighborhoods adjacent to the central business district, some of which, strictly speaking, might not even be slums.” And they needed to do it with conservatives who believed in small government ascendent. The policy synthesis that they created, with allies in academia and the government, was urban renewal.

Oakland’s native son, William Knowland, was the Senate Majority Leader, and he worked with President Dwight Eisenhower to craft the legsilation. Eisenhower wanted to prevent “the spread of blight into good areas of the community through strict enforcement of housing and neighborhood standards and strict occupancy controls,” rehabilitate “salvable areas” by improving their facilities, and enable the “clearance and redevelopment” of slums. Building on the previous Federal housing acts, and state redevelopment acts, there would be a new bill with blight as its target.

Through the summer of 1954, the House and Senate passed and reconciled their versions of the new Federal Housing Act. Unlike earlier legislation, which had gestured at large-scale public housing, Eisenhower’s legislation would leave building homes to business, as the businessmen desired. Eisenhower signed it in August. A new pool of funds became available for cities “utilizing all means available to eliminate and prevent slums and urban blight,” as one Federal administrator put it. In exchange, cities had to pass up-to-date codes and ordinances, build a comprehensive “workable” plan for developing the city, and in a sop to housing reformers, swear that they had a way to house people displaced by any “renewal” efforts. (They almost always did not.)

Urban renewal handed over massive power to local governments, but the believers in small government weren’t worried because, as legal scholar Wendell Pritchett, now the dean of the law school at the University of Pennsylvania put it, the elites “believed that condemnation would focus on a discrete group of properties that they would systematically select.” And it did.

The selection was accomplished through the technocratic declaration of an area to be blighted. Once an area had been labeled blighted, residents were deemed “less worthy of the full bundle of rights” that Americans assumed. Governments took the land through eminent domain and either built new government facilities (highways, stadiums, postal distribution outlets, other kinds of facilities) or paid to clear it, and handed it to developers. They were aided in all this by a 1954 Supreme Court decision, Berman v. Parker.

1954: Berman v. Parker

In Berman v. Parker, the Court ruled that local governments could take private property that was within an area that had been declared “blighted” and do whatever they pleased with it. Building on the landmark zoning case, Village of Euclid v. Ambler Realty Company, the justices gave cities carte blanche to do what they, apparently, needed to do to protect the health and well-being, physical and moral of their citizens.

“Miserable and disreputable housing conditions may do more than spread disease and crime and immorality. They may also suffocate the spirit by reducing the people who live there to the status of cattle,” wrote Justice William Douglas. “They may indeed make living an almost insufferable burden. They may also be an ugly sore, a blight on the community which robs it of charm, which makes it a place from which men turn. The misery of housing may despoil a community as an open sewer may ruin a river.”

What this meant, really, was that bulldozing a slum or even just a blighted area, even if some chunk of the homes or businesses within it were fine, was, in and of itself, a public good.

“The experts concluded that, if the community were to be healthy, if it were not to revert again to a blighted or slum area, as though possessed of a congenital disease, the area must be planned as a whole,” the Court held. “We think the standards prescribed were adequate for executing the plan to eliminate not only slums as narrowly defined by the District Court, but also the blighted areas that tend to produce slums.”

The Supreme Court decided Berman just months after the famous school integration case, Brown v. Board of Education. While the Brown case has been celebrated as a crowning racial achievement of the mid-century, Berman had an equal impact, but in the opposite direction. “By selecting racially changing neighborhoods as blighted areas and designating them for redevelopment, the urban renewal program enabled institutional and political elites to relocate minority populations and entrench racial segregation,” wrote legal scholar Wendell Pritchett. Combined with the all-white development of the suburbs, which was backed at every level of government, Berman helped ensure that segregation of all kinds would continue long into the future